| |

| |

Caption: UI Foundation Series - Bulletin 3 (1936)

This is a reduced-resolution page image for fast online browsing.

EXTRACTED TEXT FROM PAGE:

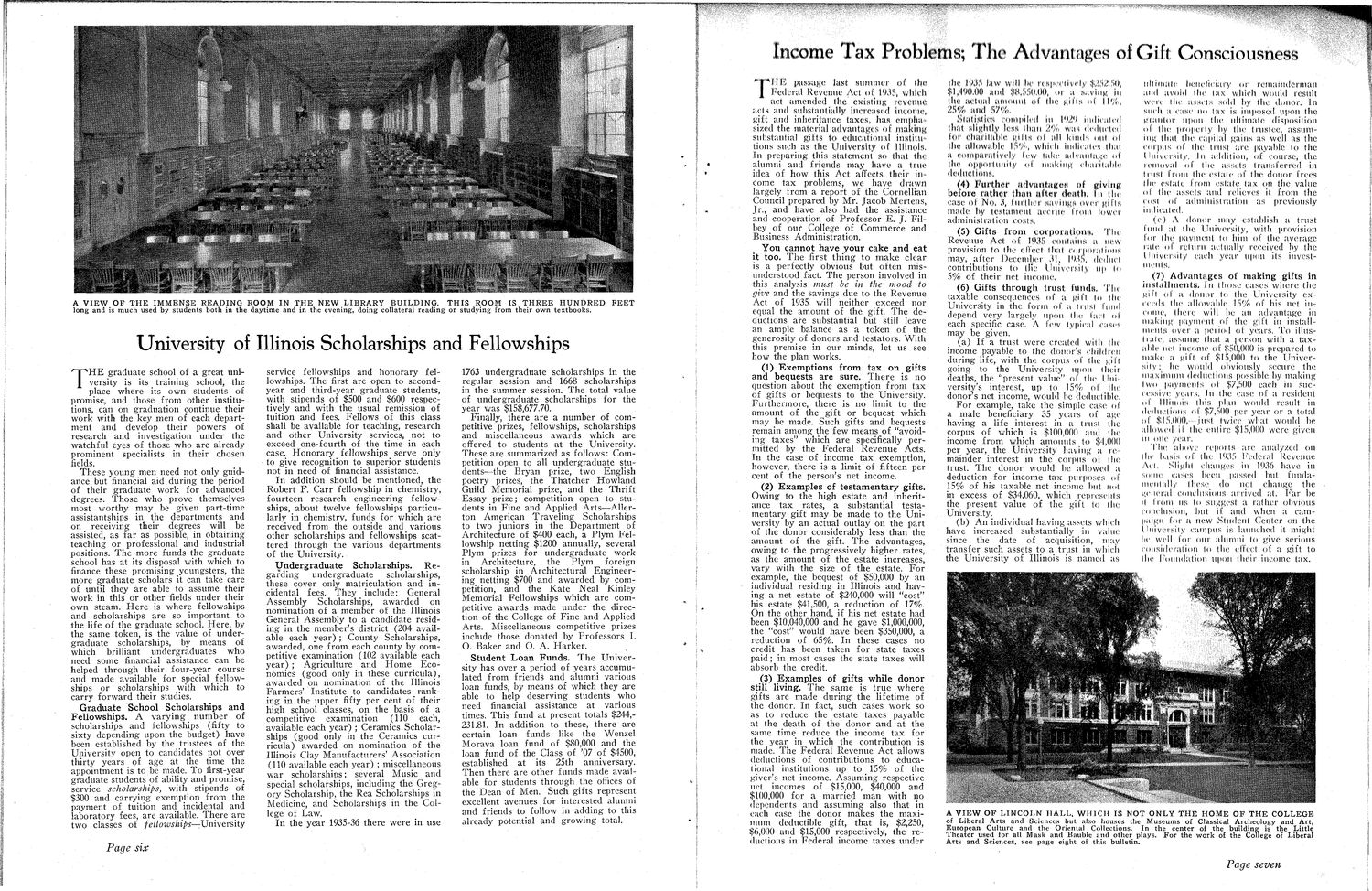

Income Tax Problems; 'Flic A d v a n c e s of Gift Consciousness NIK passage last sunuuci ol (lie federal Revenue Ac! <il l f U \ WIIK h act amended ilie existing revenue acts and substantially inci eased income, gift and inheritance (axes, lias eniplia sized the material advantages of making substantial gifts to educational instilu tions such as the University of Illinois, In preparing this statement so that the alumni and friends may have a. h u e idea of how this Act affects their in come tax problems, we have drawn largely from a report of the Corn el linn Council prepared by Mr. Jacob Mcrtetis, Jr., and have also had the assistance and cooperation of Professor E. J. Filbey of our College of Commerce and Business Administration. You cannot have your cake and eat it too. T h e first t h i n g to m a k e clear is a perfectly obvious but often misunderstood fact. T h e person involved in this analysis must be in the mood to give and the savings due to the Revenue Act of 1935 will neither exceed nor equal the amount of the gift. T h e deductions are substantial but still leave an ample balance as a token of the generosity of donors and testators. With this premise in our minds, let us see how the plan works. (1) Exemptions from tax on gifts and bequests are sure. T h e r e is no question about the exemption from tax of gifts or bequests to the University. Furthermore, there is no limit to the amount of the gift or bequest which may be made. Such gifts and bequests remain among the few means of "avoiding taxes" which are specifically permitted by the Federal Revenue Acts. In the case of income t a x exemption, however, there is a limit of fifteen per cent of the person's net income. (2) Examples of testamentary gifts. Owing to the high estate and inheritance tax rates, a substantial testamentary gift may be made to the University by an actual outlay on the part of the donor considerably less than the amount of the gift. T h e advantages, owing to the progressively higher rates, as the amount of the estate increases, vary with the size of the estate. For example, the bequest of $50,000 by an individual residing in Illinois and having a net estate of $240,000 will "cost" his estate $41,500, a reduction of 17%. On the other hand, if his net estate had been $10,040,000 and he gave $1,000,000, the "cost" would have been $350,000, a reduction of 65%. In these cases no credit has been taken for state taxes paid; in most cases the state taxes will absorb the credit. (3) Examples of gifts while donor still living. T h e same is t r u e w h e r e gifts are made during the lifetime of the donor. In fact, such cases work so as to reduce the estate taxes payable at the death of the donor and at the same time reduce the income tax for the year in which the contribution is made. The Federal Revenue Act allows deductions of contributions to educational institutions up to 15% of the giver's net income. Assuming respective net incomes of $15,000, $40,000 and $100,000 for a married man with no dependents and assuming also that in each case the donor makes the maximum deductible gift, that is, $2,250, $(),()()() and $15,000 respectively, the reductions in Federal income taxes under I the I'M . law w i l l In- M sp« . h \ , l\ :}.,",.• ',(), $1.'l«i(MHl and IfK.'.MHM), ,.i a s . m u g H I the .ii lual a i m . m i l ..I the K .ills ol I l« ,., .'V lll.lt i> and W/''IK compiled l«".«. i h a t l in ."•;• |<J,Mj 1I1(|M (| Statistics shghlly |,(| led U.I', <|r.|lK In, t l i a i i l . i l . l e Kilt-, ..I all Kind". ..ill ul the allowable I V , , \vlu< h mdi< airs that a < u i i i j M i a l i v e l v lew lake advaiilar.e ol tin- oppu! 1 1 1 1 v " I m a k i n g c hai liable 111 de<lut I inn*.. (4) F u r t h e r a d v a n t a g e ol giving before rather than a l t e r death. In tin case ol No, j , linllin sa\ nips m ei gills ma.de by testament ,u < iu< II.HII lowei administration cost'.. (5) Gifts from cm p o t a t i o n s . T h e Revenue Act of PUN contains a new provision t o t h e elVeel that « m poi ,,l s A V I E W O F T H E I M M E N S E R E A D I N G ROOM IN T H E N E W L I B R A R Y B U I L D I N G . T H I S ROOM IS T H R E E H U N D R E D long and is much used by students both in the daytime and in the evening, doing collateral reading or studying from their own textbooks. FEET University of Illinois Scholarships and Fellowships T H E graduate school of a great university is its training school, the place where its own students of promise, and those from other institutions, can on graduation continue their work with the key men of each department and develop their powers of research and investigation under the watchful eyes of those who are already prominent specialists in their chosen fields. These young men need not only guidance but financial aid during the period of their graduate work for advanced degrees. Those who prove themselves most worthy may be given part-time assistantships in the departments and on receiving their degrees will ^ be assisted, as far as possible, in obtaining teaching or professional and industrial positions. T h e more funds the graduate school has at its disposal with which to finance these promising youngsters, the more graduate scholars it can take care of until they are able to assume their work in this or other fields under their own steam. H e r e is where fellowships and scholarships are so important to the life of the graduate school. Here, by the same token, is the value of undergraduate scholarships, by means of which brilliant undergraduates who need some financial assistance can be helped through their four-year course and made available for special fellowships or scholarships with which to carry forward their studies. Graduate School Scholarships and Fellowships. A v a r y i n g n u m b e r of scholarships and fellowships (fifty to sixty depending upon the budget) have been established by the trustees of the University open to candidates not over thirty years of age at the time the appointment is to be made. T o first-year graduate students of ability and promise, service scholarships, with stipends of $300 and carrying exemption from the payment of tuition and incidental and laboratory fees, are available. There are two classes of fellowships—University service fellowships and honorary fellowships. The first are open to secondyear and third-year graduate students, with stipends of $500 and $600 respectively and with the usual remission of tuition and fees. Fellows of this class shall be available for teaching, research and other University services, not to exceed one-fourth of the time in each case. Honorary fellowships serve only to give recognition to superior students not in need of financial assistance. In addition should be mentioned, the Robert F. Carr fellowship in chemistry, fourteen research engineering fellowships, about twelve fellowships particularly in chemistry, funds for which are received from the outside and various other scholarships and fellowships scattered through the various departments of the University. Undergraduate Scholarships. Regarding undergraduate scholarships, these cover only matriculation and incidental fees. They include: General Assembly Scholarships, awarded on nomination of a member of the Illinois General Assembly to a candidate residing in the member's district (204 available each y e a r ) ; County Scholarships, awarded, one from each county by competitive examination (102 available each year) ; Agriculture and H o m e Economics (good only in these curricula), awarded on nomination of the Illinois Farmers' Institute to candidates ranking in the upper fifty per cent of their high school classes, on the basis of a competitive examination (110 each, available each year) ; Ceramics Scholarships (good only in the Ceramics curricula) awarded on nomination of the Illinois Clay Manufacturers' Association (110 available each year) ; miscellaneous war scholarships; several Music and special scholarships, including the Gregory Scholarship, the Rea Scholarships in Medicine, and Scholarships in the College of Law. In the year 1935-36 there were in use 1763 undergraduate scholarships in the regular session and 1668 scholarships in the summer session. T h e total value of undergraduate scholarships for the year was $158,677.70. Finally, there are a number of competitive prizes, fellowships, scholarships and miscellaneous awards which are offered to students at the University. These are summarized as follows: Competition open to all undergraduate students—the Bryan prize, two English poetry prizes, the Thatcher Howland Guild Memorial prize, and the Thrift Essay prize; competition open to students in Fine and Applied Arts—Allerton American Traveling Scholarships to two juniors in the Department of Architecture of $400 each, a Plym Fellowship netting $1200 annually, several Plym prizes for undergraduate work in Architecture, the Plym foreign scholarship in Architectural Engineering netting $700 and awarded by competition, and the Kate Neal Kinley Memorial Fellowships which are competitive awards made under the direction of the College of Fine and Applied Arts. Miscellaneous competitive prizes include those donated by Professors I. O. Baker and O. A. Harker. Student Loan Funds. T h e U n i v e r sity has over a period of years accumulated from friends and alumni various loan funds, by means of which they are able to help deserving students who need financial assistance at various times. This fund at present totals $244,231.81. In addition to these, there are certain loan funds like the Wenzel Morava loan fund of $80,000 and the loan fund of the Class of '07 of $4500, established at its 25th anniversary. Then there are other funds made available for students through the offices of the Dean of Men. Such gifts represent excellent avenues for interested alumni and friends to follow in adding to this already potential and growing total. may, after December M, I'U'i, de.hi. I contributions to tlie Uuiveisily up !<• 5% of their net income. (6) Gifts t h r o u g h trust I in ids. T h e taxable consequences ol a j,111 to tinUniversity in the form ol a tins! IIIIKI depend very largely upon the la< I ol each specific case. A few typical < asc •. may be given. (a) If a trust were created with the income payable to the donor's childim during life, with the corpus of the > i 11 • going to the University upon Iheii deaths, the "present value" of the Uui versity's interest, up to 15% of the donor's net income, would be deductible. For example, take the simple case of a male beneficiary 35 years of age having a life interest in a trust (he corpus of which is $100,000 and the income from which amounts to $1,000 per year, the University bavin;.', a. ie mainder interest in the corpus of tintrust. The donor would be allowed a deduction for income tax purposes of 15% of his taxable net income but uol in excess of $34,060, which represent*; the present value of the gift to the University. (b) An individual having assets which have increased substantially in value since the date of acquisition, tuav transfer such assets to a trust in which the University of Illinois is named as ultimate benefit i a i y <>i t eiuaindertuan and avoid I In- lav which would lesult wen- Ihe asset-, sold by the donor. In such a ease no tax is imposed upon the giauloi upon the ultimate disposition ol the p i o p e i t y bv the trustee, assuming that the capital gains as well as the « H I pus ol the 11 ust aie payable to the I ' 1 1 v ei silv. In a d d i t i o n , of course, the 1 i c m o v a l ol the assets I r a n s l e r r c d in t i n s ! 11 c mi the estate of the donor frees the estate l i m n estate tax on the value (d Ihe assets and iclieves it f r o m the <<»st ol adniiuisl t a t i o i i as previously indicated. ( c ) A doiioi may establish a trust I unci .it the U n i v e r s i t y , w i t h provision l o i (he payment to him of the average tale o f l e t u i u actually teeeived by the U u i v e i s i l y each year upon its invest incuts, (7) A d v a n t a g e s o f m a k i n g g i f t s i n i n s t a l l m e n t s . I n those cases w h e r e t h e g i l l ol a d o n o r to Ihe U n i v e r s i t y exceeds the allowable l ! i % of his net. i n come, Iheie w i l l be an advantage in m a k i n g payment of (he gift in installincuts over a period of years. T o illusl i a l e , assume that a person w i t h a t a x able net income o f $!i(),0()() is prepared to make a ei I t ol $I.S,()()0 to (hi! U n i v e r s i t y ; lie would obviously secure the ma M i m i m deductions possible by m a k i n g I wo payments o f $7,500 each in successive v e i l ' . , hi the case of a resident cd I l l i n o i s this plan w o u l d result in dediic lions of $7,!i()0 per year or a total cd $1SJHKI, just twice what w o u l d be allow e.| 11 (he entire $15,000 were given III o n e yea I T h e above i c p o i l s aie analyzed on lh«- basis o | (he HUN f e d e r a l Revenue Ac i Slight elianp.es in \{K\() have in some cases been passed but fundamentally these do not change the I'.cucial conclusions a r r i v e d at. bar be it I l o i n us lo suggest a rather obvious conclusion, but if and when a campaign l o i a new Student Center on the U u i v e i s i l y campus is launched it might be well l o i our a l u m n i to give serious coiisidei at ion lo the effect o f a gift, to the f o u n d a t i o n upon their income tax. Page six A V I E W O F L I N C O L N HALL, W H I C H IS NOT O N L Y T H E H O M E O F T H E C O L L E G E of Liberal Arts and Sciences hut also houses the Museums of Classical Archeology and Art, European Culture ami the Oriental Collections. In the center of the building is the Little Theater used for all Mask and Hauhle and other plays. For the work of the College of Liberal Arts and Sciences, see paj'.c eif'.ut ol this bulletin. Page seven

| |